The Chemours Company is a diversified chemical company serving multiple industries. Here are its products:

Exhibit 1:

Here's the graph of the monthly returns of the Vanguard S&P 500 Index ETF and the Chemours Company:

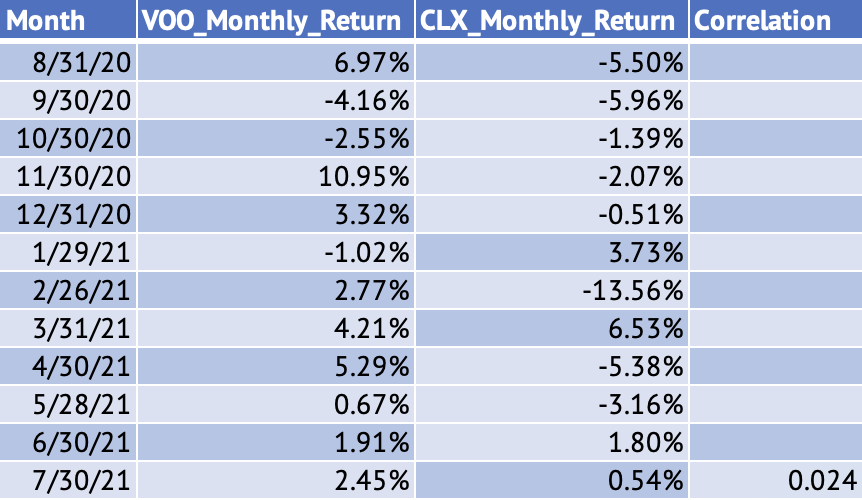

Exhibit 2:

|

| Source: Data Provided by IEX Cloud, Graph Created Using Microsoft Excel and RStudio |

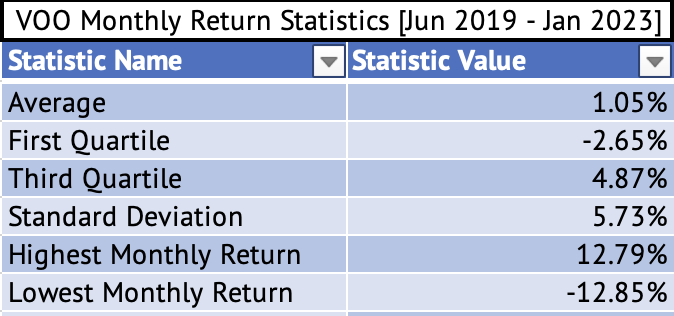

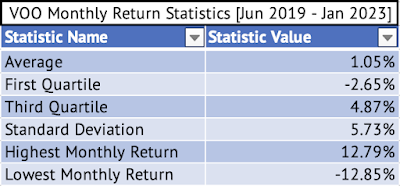

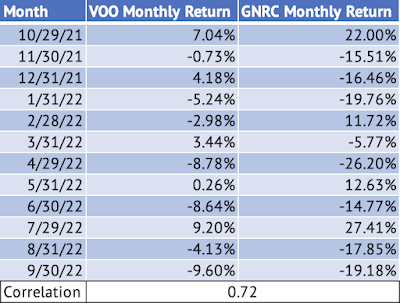

Exhibit 3:

|

| Source: Data Provided by IEX Cloud, Calculated Using Microsoft Excel |

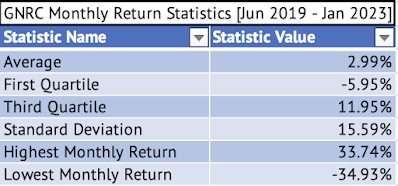

Exhibit 4:

|

| Source: Data Provided by IEX Cloud, Calculated Using Microsoft Excel |

Here's the output from the linear model:

Call:

lm(formula = CC_Monthly_Return ~ VOO_Monthly_Return, data = VOOandCC)

Residuals:

Min 1Q Median 3Q Max

-0.23930 -0.07880 0.01016 0.07621 0.29157

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.006698 0.018764 0.357 0.723

VOO_Monthly_Return 1.825643 0.325520 5.608 1.45e-06 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.1224 on 42 degrees of freedom

Multiple R-squared: 0.4282, Adjusted R-squared: 0.4146

F-statistic: 31.45 on 1 and 42 DF, p-value: 1.45e-06

The stock had a great January 2023 with a return of 18% compared to a 6.2% return of the Vanguard S&P 500 Index ETF.

Here's the chart of the monthly returns of the Vanguard S&P 500 Index and the Chemours Company:

Exhibit 5:

|

| Source: Data Provided by IEX Cloud, Calculated Using Microsoft Excel |

![Monthly Returns of Sealed Air Corp. and Vanguard S&P 500 Index ETF [June 2019 - August 2022]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEiSotWsT6tTgW3luCt3iEODsOGn6pJipMggQ7pPQGYBcAlf4iKukfkRVUeQTsczXHCcnq-UB_KpqWfO6NICzwZRHWTbICKW2ksTSfIdmfzWYYUIr90GSUdM-1qhnJEvdLRNsVhDXAAWzyOGc9w6Z_eA8TH0eMf13oaLwvQubU0-3lrLsvAe2sv0F7lu/s538/Rplot01.jpeg "Monthly Returns of Sealed Air Corp. and Vanguard S&P 500 Index ETF [June 2019 - August 2022]")