|

| Snowflake Cortex AI Product Stack (Source: Snowflake) |

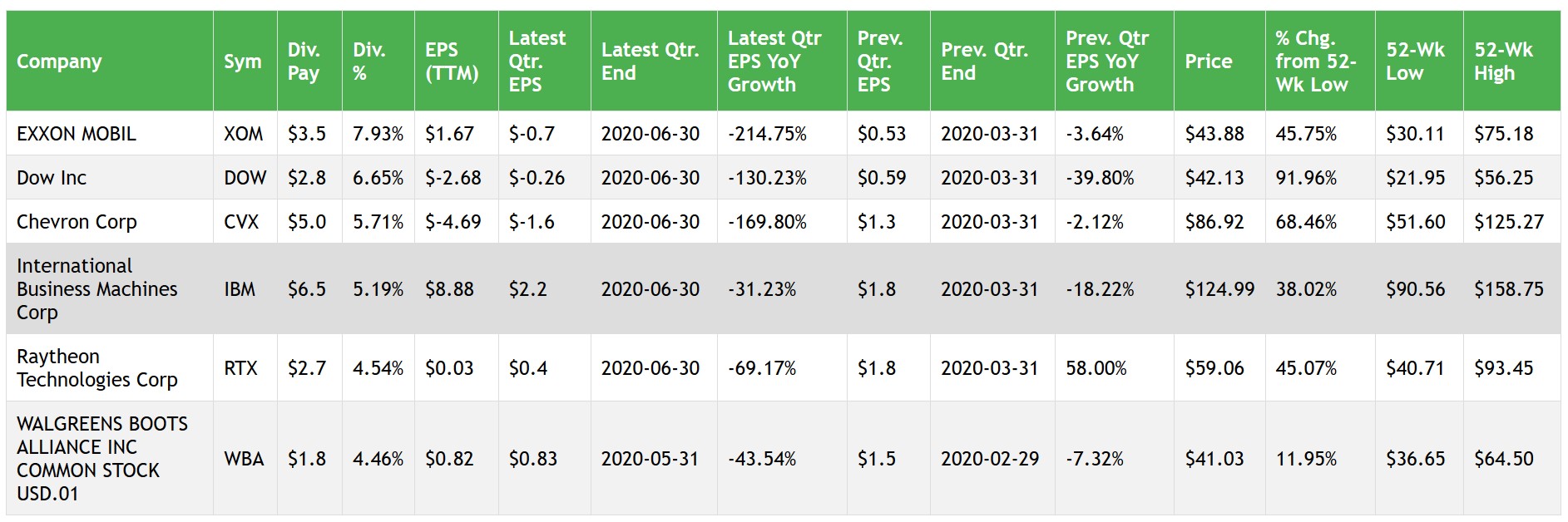

📊 Are you an asset

manager, investment professional, or anyone dealing with large volumes

of text data? Learn how to extract valuable insights from earnings press

releases, SEC filings, and other text-heavy documents in just 40

minutes!

🚀 Excited to share my new Snowflake Notebook that demonstrates the power of Snowflake Cortex LLM SQL functions!

You can download the Notebook here.

🎯 In just 30-40 minutes, discover how to:

• Classify text and assess sentiment.

• Parse and split documents efficiently

• Handle unstructured text data with ease

• Leverage Cortex Search for document Q&A

• Cortex Search is a hybrid vector and keyword search - a fascinating, easy-to-use search tool for enterprise data.

💡

Perfect for anyone wanting to explore Snowflake's LLM capabilities

without complex setups. I've used real-world examples with Earnings

Press Releases from US-listed companies to demonstrate practical

applications.

🔍 What you'll learn:

- CLASSIFY_TEXT

- COMPLETE

- EXTRACT_ANSWER

- SENTIMENT

- SUMMARIZE

- PARSE_DOCUMENT

- SPLIT_TEXT_RECURSIVE_CHARACTER functions

- Document search and Q&A using Cortex Search

⚡️ Ready to dive in? Download the notebook from Github and start your LLM journey with Snowflake today!

{kind=link}